Preparing for your child’s future starts with smart savings plans like the Registered Education Savings Plan (RESP). Understanding how to leverage its benefits can significantly impact your child’s educational financing.

At Tater, we’re dedicated to helping you navigate these waters with ease. Our guide offers practical tips for maximizing RESP contributions, ensuring a brighter future for your children.

Maximizing RESP Benefits

When planning for your child’s education, understanding the Registered Education Savings Plan (RESP) can be a game changer. This tax-advantaged savings account allows parents and guardians to invest in their child’s future education, combining flexibility with powerful financial incentives.

Tax-Free Growth and Government Contributions

One of the key benefits of an RESP is its tax-deferred status. While contributions to an RESP are not tax deductible, any investment growth within the account accumulates tax-free. This means that earnings from investments, whether interest, dividends, or capital gains, are not taxed as long as they remain within the account. This advantage alone can significantly enhance the savings growth over time.

Additionally, the government offers generous grants to boost your savings. The Canada Education Savings Grant (CESG) adds 20% to the first $2,500 contributed annually per child, which amounts to up to $500 a year, maxing out at $7,200 over the plan’s lifetime. Understanding and leveraging these grants is essential for maximizing your contributions. Starting early and contributing regularly to meet the annual limit can ensure you receive the full CESG benefit.

Strategic Contributions for Maximum Impact

Strategically planning your contributions can significantly impact the fund’s growth. Here are a few tactics:

- Start Early: The sooner you start contributing, the more time your investment has to grow. Early contributions also ensure you maximize government grants.

- Consistent Contributions: Regular contributions, even in small amounts, can grow significantly due to compound interest and consistent government matching.

- Maximize Government Grants: Aim to contribute at least $2,500 per year to secure the maximum CESG. If you’re catching up on missed contributions, you can contribute up to $5,000 a year per child to receive past grants.

- Utilize Family Plans for Multiple Children: Family plans allow you to spread the grant money across siblings, providing flexibility in fund allocation and potentially maximizing the benefits if one child decides not to pursue post-secondary education.

Remember, the impact of these contributions extends beyond just the financial. By securing funds for their education, you’re also providing your children with peace of mind, enabling them to focus on their studies without the burden of financial stress. Moreover, introducing your child to the concept of saving and investing early on can foster financial literacy and responsibility from a young age.

For detailed tips on saving and investing, consider visiting smart budgeting for families and building a balanced portfolio. These resources can provide additional guidance on making informed decisions that align with your financial goals and your child’s educational aspirations.

Boosting RESP Contributions

Strategically timing and planning your contributions to a Registered Education Savings Plan (RESP) can substantially increase the funds available for your child’s post-secondary education. Here’s how you can maximize your RESP contributions effectively.

Timing Your Contributions

The first step towards maximizing your RESP contributions involves strategic timing. Contributing early in the year or right at your child’s birthday can make a significant difference. By doing so, you’re not only giving your investments more time to grow but also ensuring you don’t miss out on the annual government grants due to procrastination or oversight.

- January Contributions: Contributing in January takes advantage of the entire year’s growth potential.

- Birthday Contributions: Aligning contributions with your child’s birthday makes it memorable and manageable.

Catch-Up Contributions

Life happens, and there might be years when you cannot contribute to an RESP. Fortunately, catch-up contributions are an option, allowing you to contribute for previous years and still receive the government grant. However, it’s essential to note that the government matches 20% up to $500 per year, with a maximum of $1,000 if you’re catching up (for a contribution of $5,000).

- Double Up: If possible, double your contributions to $5,000 for one child in any given year to catch up on missed CESG.

- Plan Ahead: Catching up requires careful planning to not over-contribute or miss other children if you have a family plan.

Family Plans and Multiple Children

A Family RESP Plan is a fantastic way to manage savings for families with more than one child. This plan allows you to allocate funds to different children as needed, which can be particularly useful if one child decides not to pursue post-secondary education.

- Flexibility: A family plan provides flexibility in fund allocation without affecting the total CESG each child can receive.

- Simplicity: Managing one plan for all children simplifies tracking your investments and government grants.

Incorporating these strategies ensures your RESP contributions work as hard as you do for your child’s future. Timely contributions, taking advantage of catch-up opportunities, and choosing a family plan for multiple children can significantly boost the amount accumulated by the time they’re ready for post-secondary education.

For families looking to dive deeper into the ins and outs of investing, the best choice between ETFs and stocks and the art of atrategic asset allocation offer strategies and tips.

Smart RESP Investment Strategies

Optimizing your Registered Education Savings Plan (RESP) isn’t just about how much you contribute, but also where you invest that money. The goal is to grow your contributions over time, ensuring you maximize the funds available for your child’s education. Here’s how to strategically approach investing within your RESP.

Diversify Your Investments

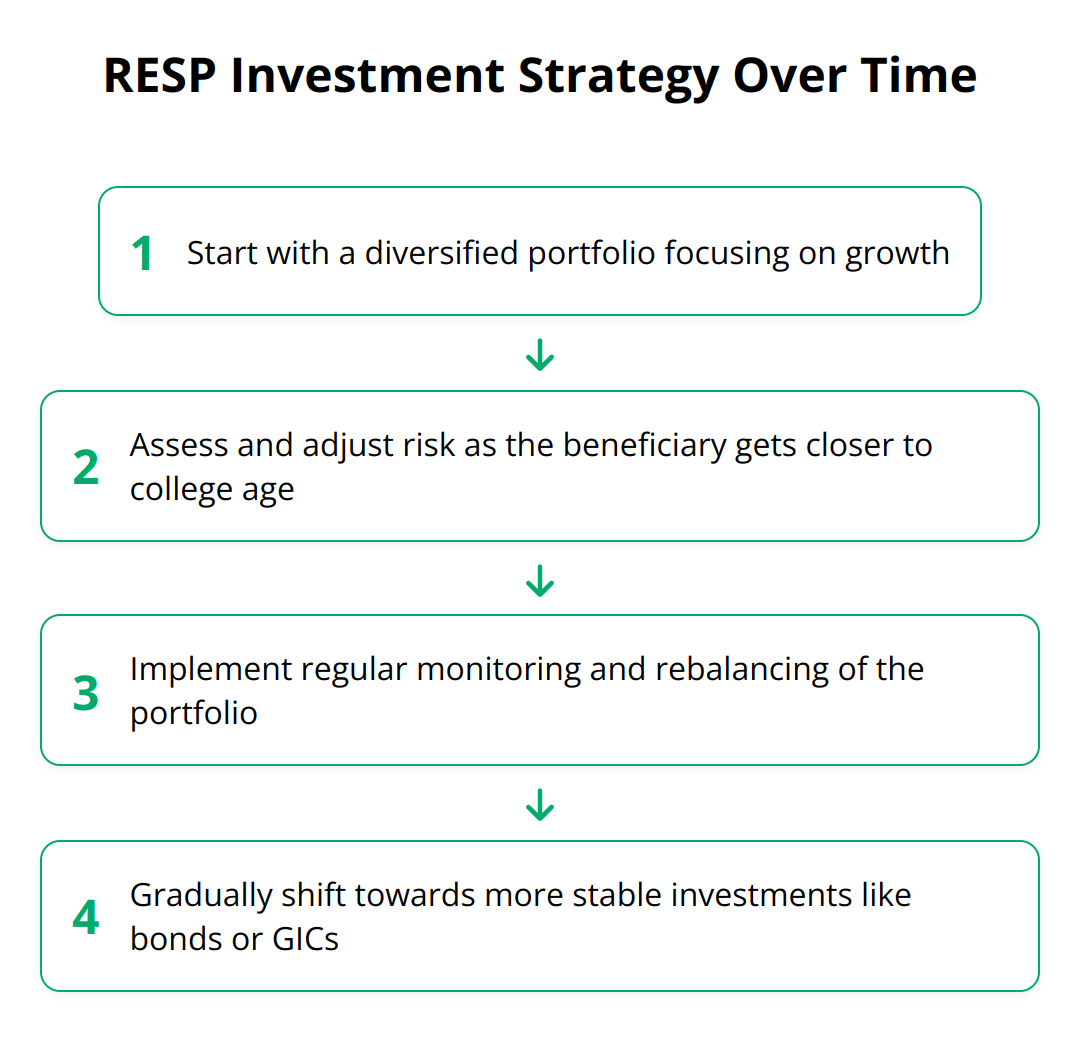

Putting all your eggs in one basket rarely works out well in the investment world, and the same holds true for RESPs. Diversifying your investment across different asset classes like stocks, bonds, and GICs can help mitigate risk. It’s not just about risk management; different investment types can offer varying rates of return over time. For instance, equities might offer higher growth potential, which is ideal in the early years of your RESP. As your child nears college or university, shifting towards more stable investments like bonds or GICs can help preserve the capital.

Risk Assessment Over Time

An RESP is a long-term investment, and your risk tolerance should evolve as the beneficiary gets closer to needing the funds. Initially, you might be comfortable with a higher-risk, higher-reward strategy. However, as the time to withdraw the funds approaches, it’s wise to lower your risk level to protect your investment from market volatility. This gradual shift ensures that by the time your child is ready for post-secondary education, your RESP is not only healthy but also not subject to a sudden dip in value due to market fluctuations.

Regular Monitoring and Rebalancing

An often overlooked aspect of RESP management is the need for regular monitoring and rebalancing. Markets change, and so will the composition of your portfolio. What started as a balanced fund can become more heavily weighted towards a specific asset class over time. Periodically reviewing your investments allows you to rebalance your portfolio, ensuring that it remains aligned with your desired risk level and investment strategy. For those not comfortable doing this themselves, you can sign up for our course where we provide all of the tools and resources you need to manage a professionally developed investment portfolio with ease.

- Tip 1: Aim to review your RESP portfolio at least annually.

- Tip 2: Consider a larger equity position early in the RESP lifecycle, gradually transitioning to bonds and GICs as your child approaches college age.

- Tip 3: Use government grants and contributions efficiently by investing them into growth-oriented assets early on.

Following these strategies can help ensure that your RESP is not just a savings account but an actively managed investment portfolio geared towards maximizing your child’s educational funds. Remember, the key is not just in saving but in smart investing within your RESP.

Final Thoughts on Building a Robust Education Fund

Maximizing Registered Education Savings Plan (RESP) contributions stands out as a pivotal strategy for securing your child’s academic future. The compounded benefits of tax-free growth, government grants, and strategic investment choices can significantly amplify the value of your savings, resulting in a substantial education fund. It’s not just about saving; it’s about smart saving and making each dollar work effectively towards your child’s education.

![Key Takeaways - RESP Contributions Maximization [Pro Tips]](https://mytater.ca/wp-content/uploads/2024/04/RESP_Contributions_Maximization__Pro_Tips__5_2024_04_16_07_12_01_824270_00_00.png)

We at Tater encourage a proactive approach to RESP contributions. Starting early, making consistent contributions, and understanding how to best leverage government grants and investment strategies can make a world of difference. It’s about foresight and planning for your child’s future today. A well-funded RESP can relieve the financial pressure of post-secondary education, allowing your children to focus on their studies and career goals.

Building a robust education fund requires more than just contributions; it requires a strategy. That’s where investment knowledge becomes invaluable. The Tater Course is designed to empower you with the expertise needed to make informed investment decisions, not just for RESPs but across all your financial endeavors. Our course offers a practical step-by-step guide and essential tools to help you invest using professional strategies and manage your investments efficiently. By eliminating management fees, our clients experience significant long-term savings, making the investment journey more rewarding and impactful.

For those looking to enhance their investment strategies and maximize their educational savings, we invite you to explore what the Tater Course has to offer at Tater Investment Solutions Inc.. Join the ranks of satisfied customers who have taken control of their financial future and are building a solid foundation for their children’s education.

In conclusion, focusing on RESP contributions and utilizing effective investment strategies can substantially benefit your child’s educational prospects. By being proactive, strategic, and knowledgeable, you can create a fund that significantly eases the financial burden of post-secondary education. Let’s not leave your child’s future to chance. Take action today and make informed decisions that will pave the way for their success.