Planning for the future is essential, especially for individuals with disabilities and their families. At Tater, we recognize the significance of understanding financial tools that can aid in this planning. The Registered Disability Savings Plan (RDSP) is one such tool, offering unique benefits and government support. In this blog post, we’ll guide you through everything you need to know about RDSPs, from opening an account to making the most of your contributions and understanding withdrawal implications.

Understanding RDSPs

The Registered Disability Savings Plan (RDSP) is a powerful financial tool designed to secure the future of individuals with disabilities. Navigating the RDSP can be complex, but with the right information, you can make informed decisions to maximize your benefits.

Breaking Down RDSP

An RDSP is not just any savings account. It is a specialized plan that offers long-term financial security for people with significant and prolonged disabilities. What sets RDSPs apart is the generous government grants and bonds that can significantly increase your savings. The plan allows for tax-deferred growth, meaning you only pay taxes on withdrawals, allowing your investments to grow more efficiently over time.

Key Eligibility Requirements

To take advantage of an RDSP, there are specific criteria that must be met:

- Canadian residency: You must have a valid Social Insurance Number and be a resident of Canada.

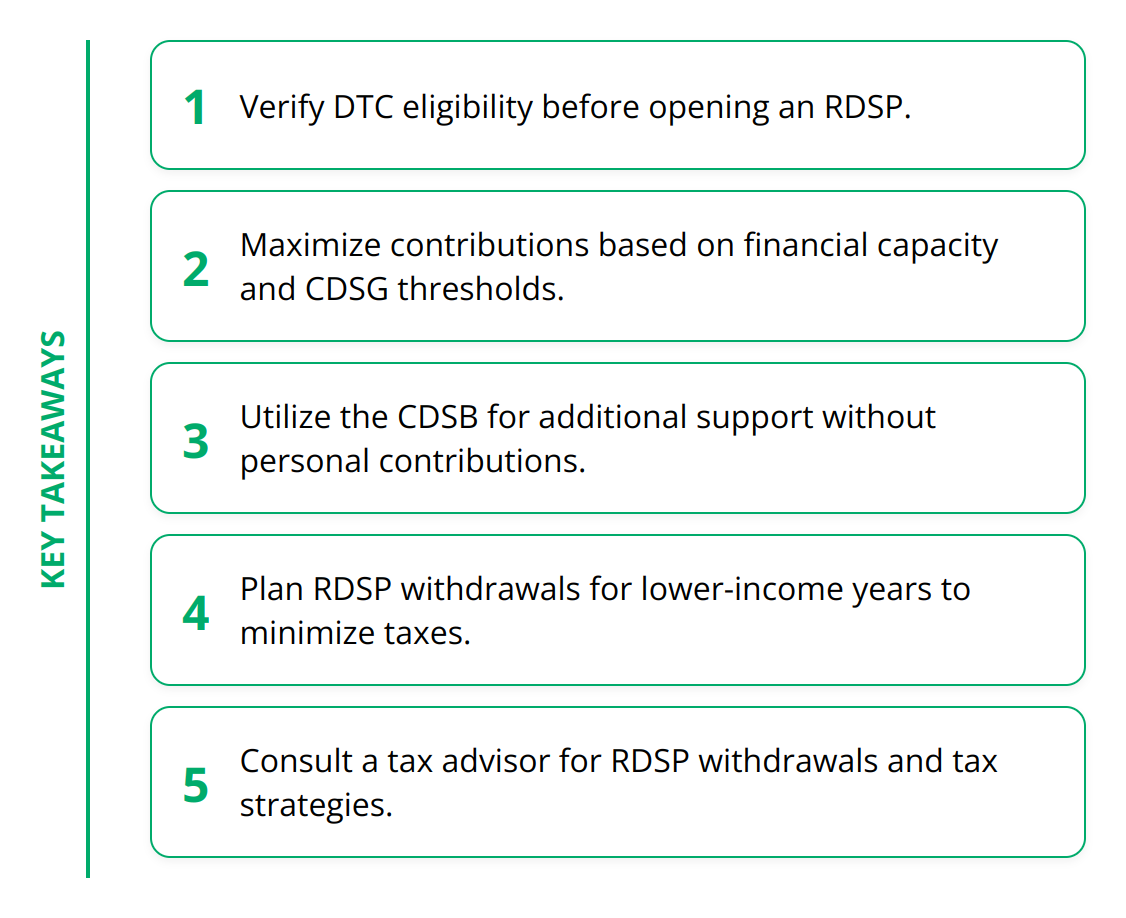

- Disability Tax Credit (DTC) eligibility: Having approval for the DTC is a gateway to opening an RDSP.

- Age restrictions: The RDSP can be opened for any eligible individual under the age of 60.

Opening an RDSP Account: Step by Step

Opening an RDSP requires diligent preparation, but following these steps can streamline the process:

By focusing on these practical steps and navigating the RDSP with a strategic approach, you can secure financial stability for the future. Always remember, starting early can make a substantial difference in the growth of your RDSP account. For more detailed guidance on managing risk in your investments, our post on managing risk is an indispensable resource.

The journey to opening and maximizing an RDSP might seem daunting at first, but equipped with the right knowledge and resources, you can ensure financial security and peace of mind for yourself or your loved ones with disabilities. Stay proactive and informed to make the most out of your RDSP.

Making Contributions Work for You

When it comes to maximizing the value of a Registered Disability Savings Plan (RDSP), understanding how contributions and government incentives work is key. Your approach to contributing to an RDSP and leveraging government grants and bonds can significantly impact the long-term growth of the plan. Here we outline some actionable insights and tips to make contributions work in your favor.

Contributions: The Backbone of RDSP Growth

Contributions to an RDSP are not tax-deductible, but they do grow tax-deferred, meaning you won’t pay tax on the investment income or growth inside the RDSP until funds are withdrawn. Notably, there’s no annual contribution limit, but there’s a lifetime contribution limit of $200,000, allowing for considerable flexibility in how and when you contribute. It’s wise to plan your contributions based on your financial capacity and future needs, keeping the lifetime limit in mind.

A strategic approach involves assessing your budget to determine consistent contribution amounts, whether monthly, quarterly, or annually. The sooner you start contributing, the more your investment can grow due to the power of compounding interest.

The Canada Disability Savings Grant: Boosting Your Contributions

The Canada Disability Savings Grant (CDSG) is a potent tool for accelerating RDSP growth. For every dollar contributed, the government can match up to 300%, depending on the beneficiary’s family income. The maximum grant is $3,500 per year, with a lifetime limit of $70,000, available until the year the beneficiary turns 49.

Maximizing the CDSG involves being aware of the income thresholds and planning contributions to get the highest possible match. Observing these thresholds and adjusting your contributions accordingly can significantly enhance the RDSP’s value over time. For detailed insights into leveraging the CDSG, consider exploring resources like our article on Fee Based Financial Advisors. Such advisors can provide help planning and strategizing contributions.

The Canada Disability Savings Bond: Additional Support for Low-Income Families

For RDSP beneficiaries from low-income families, the Canada Disability Savings Bond (CDSB) provides up to $1,000 a year without requiring any personal contributions. The lifetime limit for the bond is $20,000, accessible until the beneficiary turns 49. This is particularly beneficial for those who might not have the financial leeway to make regular contributions.

Eligibility for the CDSB is determined solely by family income, so it’s essential to submit your taxes annually to potentially qualify. For families or individuals on a tight budget, the bond is an invaluable asset, as it contributes to the RDSP’s growth without any financial burden.

In summary, effectively leveraging contributions, grants, and bonds requires a blend of strategic planning and understanding of the RDSP framework. Here are some actionable tips:

- Start Early: Begin contributing as soon as possible to take advantage of compound growth.

- Plan Contributions: Work contributions into your budget and aim for consistency.

- Maximize the CDSG: Keep abreast of income thresholds and adjust contributions to get the highest match.

- Leverage the CDSB: Ensure eligibility for the bond by keeping income information up to date.

By adopting these strategies, beneficiaries and their families can significantly enhance the impact of their RDSP, providing a robust financial foundation for the future.

RDSP Withdrawals Insight

Understanding when and how you can withdraw funds from your Registered Disability Savings Plan (RDSP) is as important as knowing how to contribute to it. The flexibility and conditions surrounding withdrawals are designed to ensure that RDSP serves its purpose—providing long-term financial security for individuals with disabilities. Here’s what you need to consider regarding RDSP withdrawals.

RDSP withdrawals mainly fall into two categories: Lifetime Disability Assistance Payments (LDAPs) and Disability Assistance Payments (DAPs). LDAPs are periodic payments that must begin by the end of the year in which the beneficiary turns 60 but can start sooner. DAPs, on the other hand, can be requested anytime but are subject to certain restrictions to prevent depletion of RDSP funds.

Timing is critical when it comes to making withdrawals. One crucial fact to remember is that withdrawals should ideally be planned when the beneficiary’s income is expected to be lower, since withdrawal amounts are considered income for tax purposes. If withdrawals are made too early or when the beneficiary’s income is higher, the tax implications could significantly reduce the benefit of the RDSP.

Tax implications are a vital aspect of RDSP withdrawals. While contributions to RDSP are not taxed upon withdrawal, the government grants, bonds, and investment growth within the RDSP are taxable. It means that strategic planning is necessary to minimize the tax hit. A common strategy is to spread out withdrawals over several years to keep annual income lower and hence, remain in a lower tax bracket.

Here are some practical steps to manage RDSP withdrawals effectively:

- Start planning early: Look ahead and project when you’ll need the funds and what your other sources of income might be.

- Consult a tax advisor: Because of the complexities around RDSP withdrawals and taxation, getting professional advice can save you a significant amount in taxes.

- Keep an eye on the rules: Government policies regarding RDSPs can change, affecting how and when you should make withdrawals.

For beneficiaries and their families, understanding these factors is key to maximizing the RDSP’s benefits. While RDSPs are designed with a long-term perspective, life circumstances can change, making it necessary to adjust your withdrawal strategy. Always stay informed about your RDSP and consider changes in income, health, and personal needs when planning withdrawals.

For further information on managing RDSP funds and navigating tax implications, visiting index investing can provide additional insights into making the most of your investments, including those within an RDSP.

Final Thoughts

The journey through understanding and utilizing the Registered Disability Savings Plan (RDSP) emphasizes its significant role in financial planning for individuals with disabilities and their families. The RDSP stands out as a beacon of hope, offering a structured pathway to securing financial stability and peace of mind. Through strategic contributions and leveraging government incentives such as grants and bonds, RDSP holders can witness the power of long-term savings and investment growth.

At Tater, we strongly believe in the transformative power of informed financial planning. The RDSP is a prime example of how understanding and accessing the right financial tools can make a profound difference in individuals’ lives. We encourage eligible individuals and families not to miss out on the immense benefits RDSPs offer. Taking the step to open and contribute to an RDSP can provide financial security and support that enhances quality of life and ensures well-being for years to come.

Moreover, in your financial journey, knowledge is as valuable as your investments. We invite you to explore our blog and Youtube channel , where we provide comprehensive guidance and tools to manage your investments effectively. Additionally, you can make our My Tater Course yours and learn how to duplicate many popular Robo-Advisor portfolios and save all the fees. Cutting these fees can increase your portfolio by a lifechanging amount, often by well over 6 figures over the long term! Join the many satisfied customers who have taken control of their financial futures with our help.

Embracing financial planning through resources like the RDSP and educating yourself on investment strategies can unlock new possibilities for financial freedom and security. We are here to support you every step of the way, providing resources and expertise to navigate the complexities of investment and savings.

In conclusion, the RDSP is an essential tool in the financial planning toolkit for those with disabilities, offering substantial benefits and support. By actively engaging with this plan and seeking out educational resources for broader financial understanding, you can lay a solid foundation for a secure financial future. Let’s make informed financial decisions today for a brighter tomorrow.